By Sam Miller, CFA® , CFP® , CAIA®

Senior Investment Strategist

At the beginning of this year, we noted that with President Biden in office and a democratic majority in Congress, tax policy changes likely would be forthcoming—but both specifics and timing remaining critical unknowns. President Biden campaigned on promises of infrastructure spending and social programs, paid for by new tax revenues on corporations and wealthy households. Months have passed since those proposed programs were announced, but the Senate finally appears ready to act on a bipartisan infrastructure bill and a broader fiscal package.

While the details are still in flux, it appears that the $550b infrastructure bill would include funding for transportation, water, and broadband, but significantly less in the way of clean energy provisions than initially proposed. Simultaneously, the Senate is considering a budget resolution that calls for $3.5 trillion in new spending over ten years—financed primarily through tax increases. There remains a strong likelihood that these amounts will be scaled back by more moderate Democrats due to concerns regarding deficits and tax increases. Striking the right balance on the spending package will be particularly difficult since it has no Republican support; instead, Democrats will attempt to pass it through a special budgetary procedure call ‘reconciliation.’

In terms of timing, the infrastructure bill could potentially pass the House by September, with the broader spending bill passing later in the year. As both plans move to the Senate, with the current 50-50 split between Democrats and Republicans, legislators will be walking a tightrope to get a deal done but we anticipate the passage of some legislation before year-end.

Looking ahead

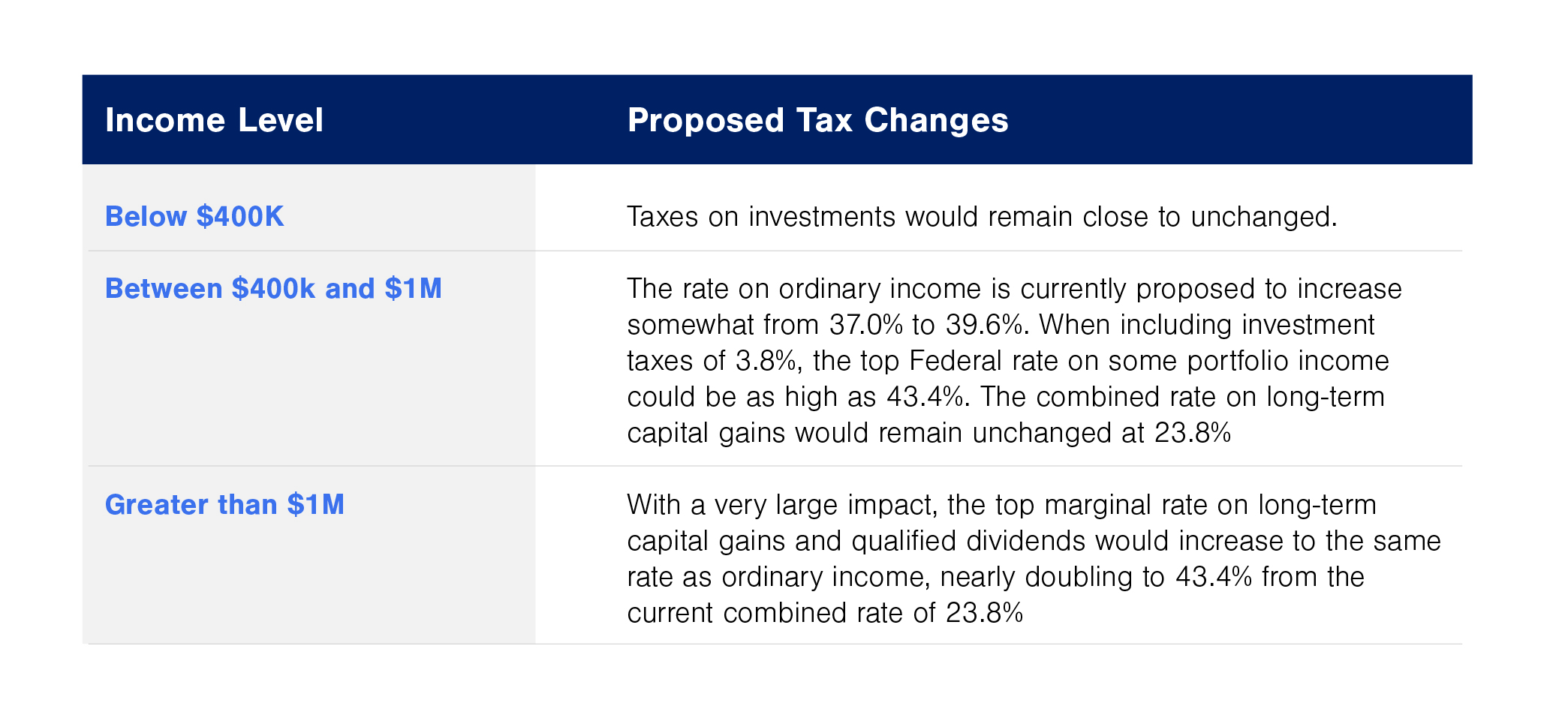

So what will this mean for investors? At a high level, the potential impact to your wealth depends to a great extent on your taxable income level. The tax brackets for each filing status and exact rates continue to be debated, but potentially may look something like this:

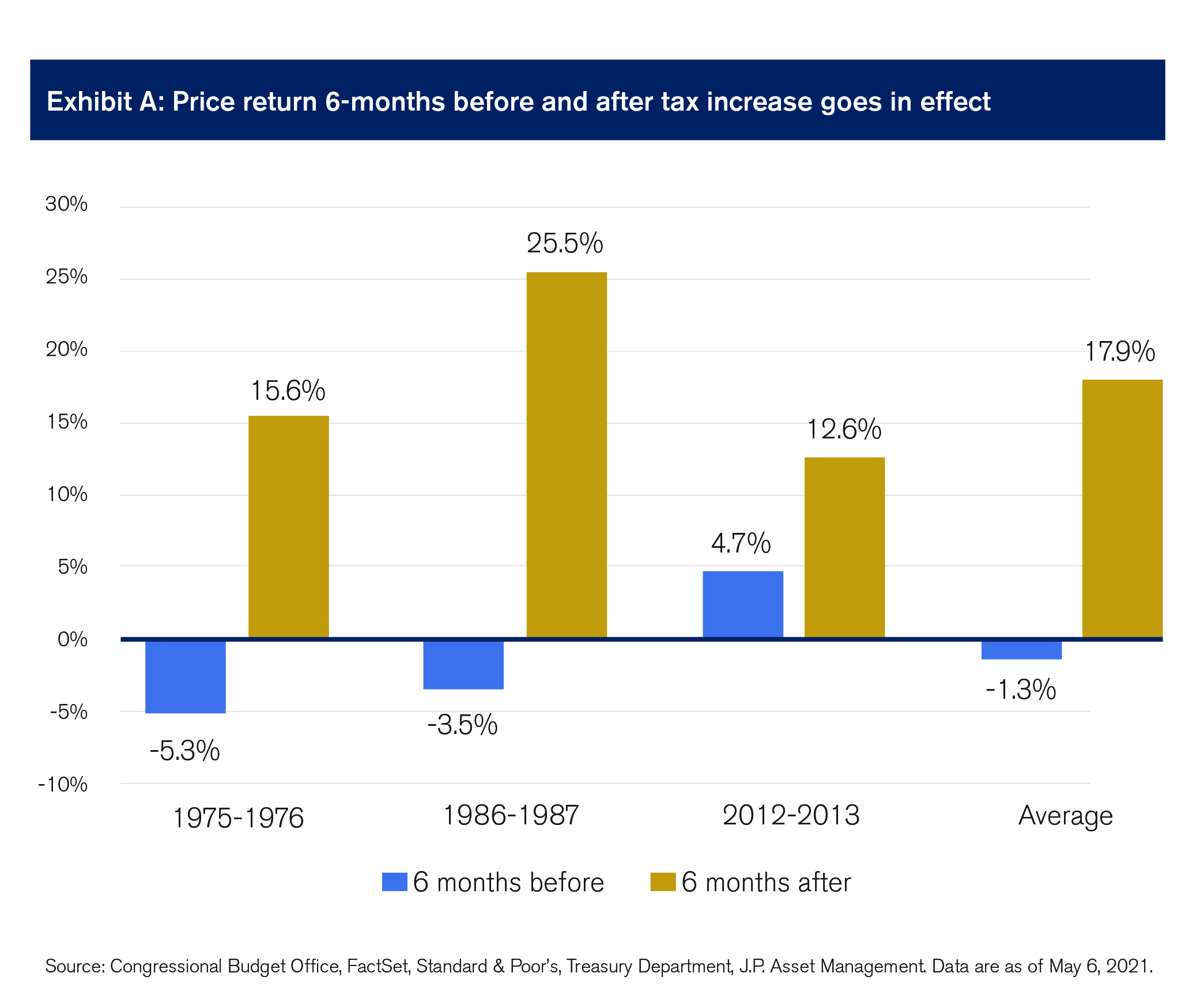

While the prospect of higher capital gains taxes can seem daunting, markets tend to take these types of tax code changes in stride. Long-term capital gains taxes have increased three times since 1970. In two of those instances, equities came under pressure in the six months leading up to the tax increase. But in all three cases, stocks rose during the six months following the tax hikes (Exhibit A). The simple truth is that while increases in the capital gains tax may pull forward some selling, they typically do not create new selling. Ultimately, the pace of economic activity and trends in corporate profitability are far more important drivers of market performance.

As the details continue to get ironed out, we’ll be keeping a close eye on developments in Washington and how any changes might impact our clients. In the meantime, there are several tools and strategies you may want to consider to begin preparing your portfolio. These include more detailed tax and estate planning, tax loss/gain harvesting, evaluating asset location, increasing your municipal bond allocation, and more.

As we gain greater tax plan clarity in the coming weeks and months, we welcome the opportunity to work with you on developing a mitigation strategy as part of your overall financial and investment plan.

For details on the professional designations displayed herein, including descriptions, minimum requirements, and ongoing education requirements, please visit www.signatureia.com/disclosures. Signature Investment Advisors, LLC (SIA) is an SEC-registered investment adviser; however, such registration does not imply a certain level of skill or training and no inference to the contrary should be made. Securities offered through Royal Alliance Associates, Inc. member FINRA/SIPC. Investment advisory services offered through SIA. SIA is a subsidiary of SEIA, LLC, 2121 Avenue of the Stars, Suite 1600, Los Angeles, CA 90067, (310) 712-2323, and its investment advisory services are offered independent of Royal Alliance Associates, Inc. Royal Alliance Associates, Inc. is separately owned and other entities and/or marketing names, products or services referenced here are independent of Royal Alliance Associates, Inc.